Vol. 2, No. 7

On the cost of capital. Corporate shuffleboard. Credit creation, cause & effects. A requested valuation of a popular burrito chain. And, value in a diamond jewellery retailer.

Valuabl is an independent, value-oriented journal of financial markets. Delivered fortnightly, Valuabl helps contrarians pop bubbles, buy low, and sell high.

HOUSEKEEPING

All valuations and investment ideas are now organised in a searchable archive. Paid subscribers have unfettered access here.

In today’s issue

The cost of capital (5 minutes)

Corporate shuffleboard (4 minutes)

Credit creation, cause & effect (5 minutes)

Requested valuations (18 minutes)

Investment ideas (21 minutes)

The cost of adultery crisis

The cost of capital

Interest rates capital costs are the most consequential yet misunderstood prices in capitalism, connecting the future to the present.

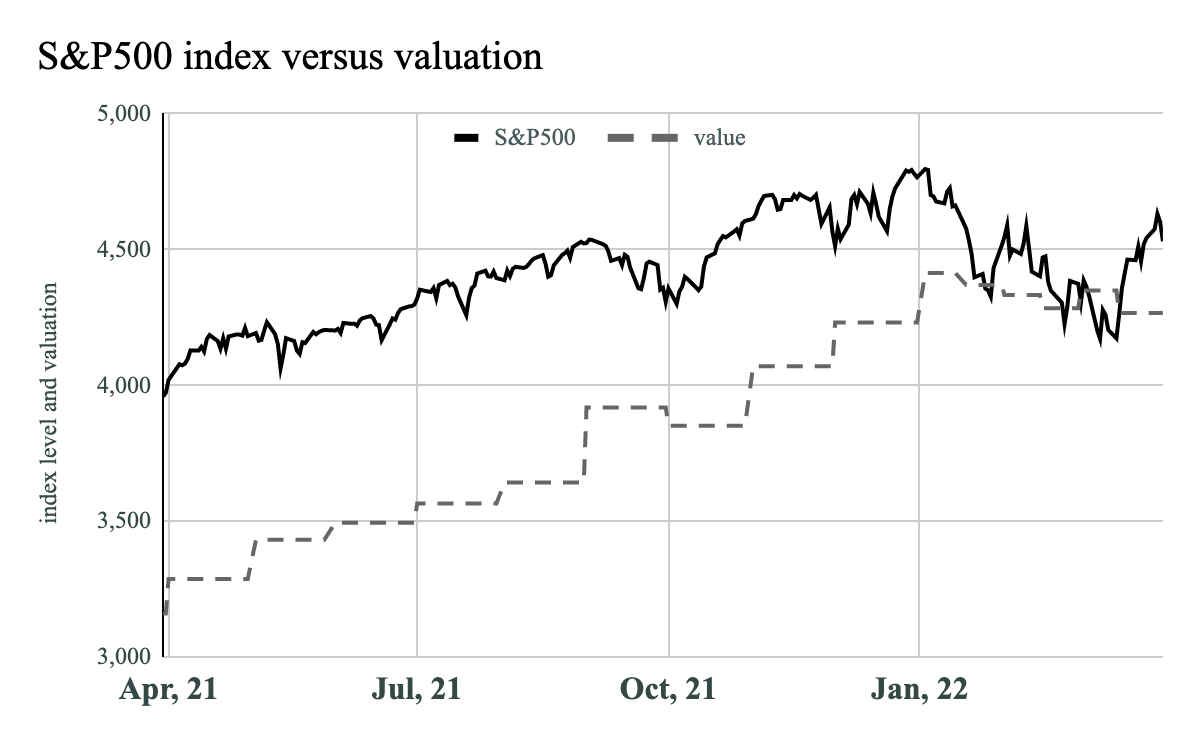

U.S. stock prices reversed their decline and rose last fortnight. The S&P500, an index of large U.S. companies, surged 8.6% to 4,530. It was at a 6-month low of 4,173 on March 15. The index is down 4.9% for the year but is up 14.5% over the last 12-months.

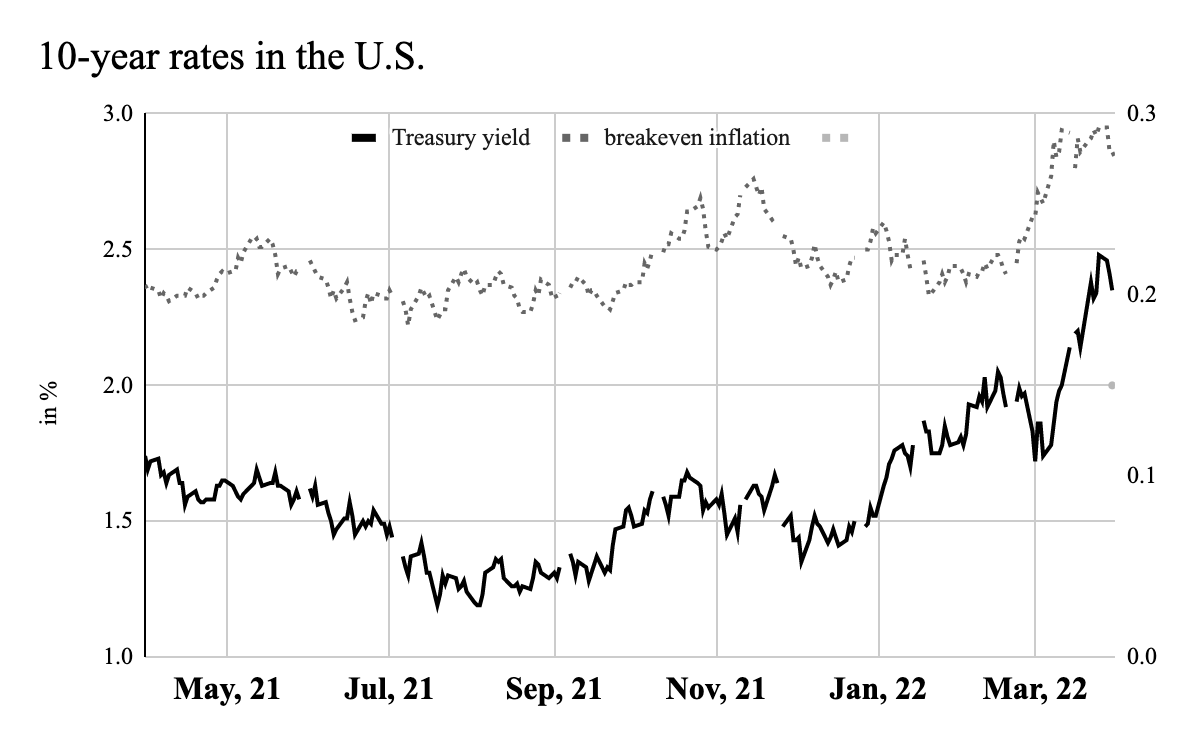

The price of 10-year U.S. Treasury notes dropped again, increasing yields. Yields peaked at 2.48% on March 25, their highest point in three years, before declining to their current level of 2.35%. In contrast, the 10-year breakeven rate declined slightly. The rate was 2.93% at the time of the last publication and now sits at 2.84%. These are still historically high levels of expected inflation, and roughly the highest level since the Federal Reserve began reporting this data in 2003. As real yields, the difference between expected inflation and nominal yields, are still negative, investors in these bonds remain willing to lose purchasing power over the next decade.

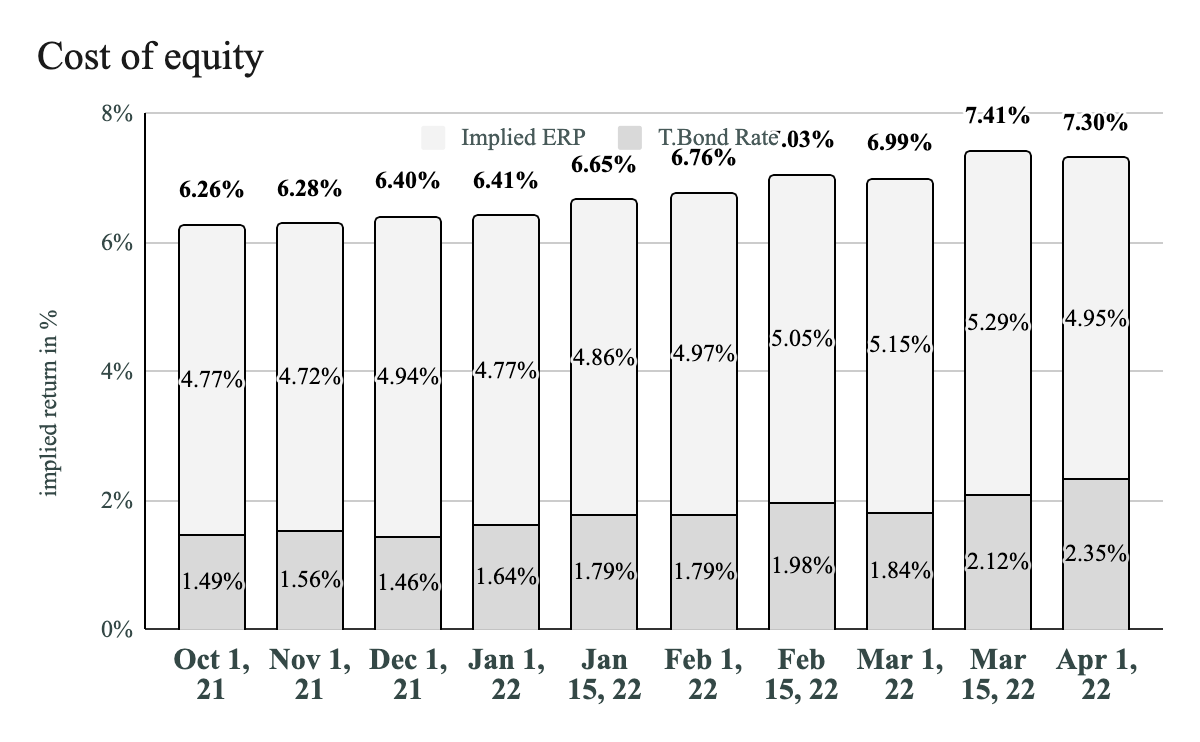

The equity risk premium dropped by 34bp as equity investors gained confidence and bid up prices. But, investors still think U.S. equities are 53bp riskier than they were 12-months ago. The cost of equity, and the implied return, for U.S. stocks declined too. Stocks are now offering implied returns of 7.30%, down from 7.41% last fortnight. While risk-free rates are at historically low levels, the 13th percentile of data going back to 1960, equity risk premiums are above average at the 71st percentile of data in that range.

While equity risk premiums were dropping, so too were spreads on U.S. corporate debt. The average spread on corporate bonds over 10-year Treasury bonds fell by 45bp. Spreads at the riskier end of the curve fell by more than the safe end as investors gained confidence. Spreads on AAA-rated bonds fell by 21bp, while BBB fell by 26bp and CCC by 81. Investors reckon corporate debt is getting safer.

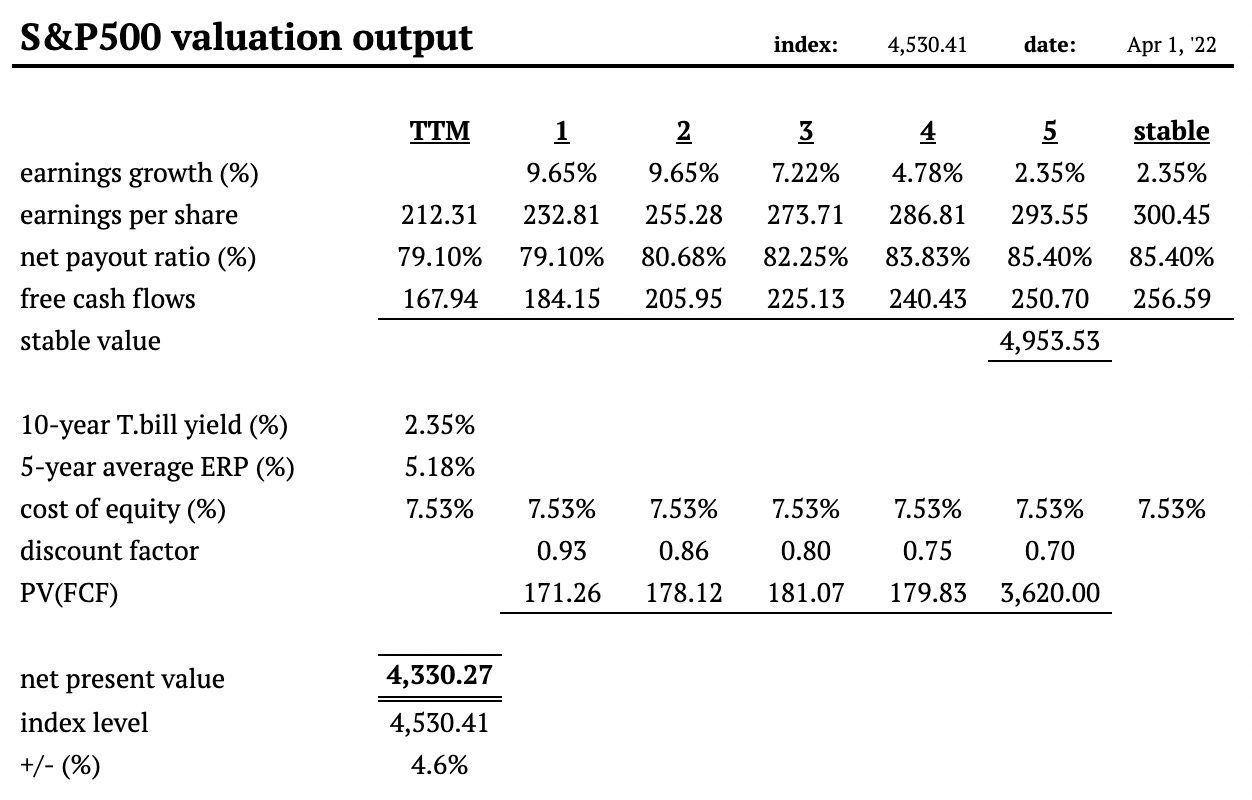

Using the average ERP of the last 5-years, the current 10-year T.bill yield, analysts’ consensus earnings estimates, and a stable payout ratio based on the S&P500’s average return on equity over the last decade, I value the index at 4,330 compared to its level of 4,530.

This valuation suggests the S&P500 index is 4.6% overvalued compared to 8% overvalued at the start of the year and 22% overvalued 12-months ago.

READY FOR MORE?

Valuabl is a reader-supported publication. To receive new issues and support independent research, consider becoming a free or paid subscriber.